[미국 생활] [영어] HSA (Health Spending Account) vs FSA (Flexible Spending Account) 다른점 비교

미국에서 세금 절감을 위해 여러가지 제도가 존재합니다. 그 중 하나인 의료비 목돈 지출과 감세 효과를 위한 HSA와 FSA가 있습니다. 오늘은 이 내용에 대해 정리 해 봅니다.

이 글은 Pinnacle Health & Benefits Account Manager Ferne Emery의 글을 번역했고 이해를 위해 사족을 조금 추가했습니다.

Ferne Emery는 Pinnacle의 Health & Benefits 팀의 계정 관리자입니다. 그녀는 NC Highpoint에 있는 Pinnacle's Premier 사무실에 있으며 전화 (336) 881-3209 와 이메일 Emery@pnfp.com을 통해 연락할 수 있습니다.

HSA와 FSA의 차이점은 무엇일까요?

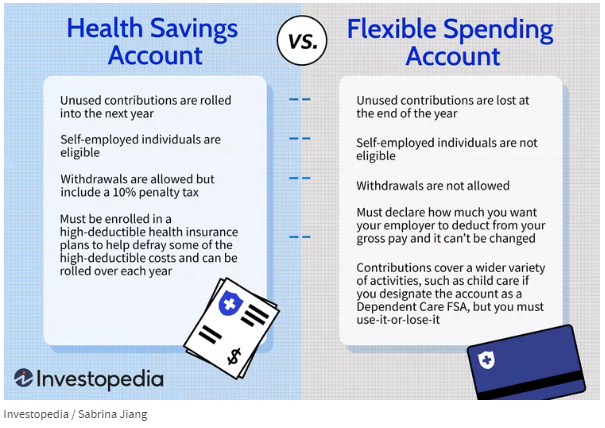

HSA(Health Savings Accounts)와 FSA(Flexible Spending Accounts)는 모두 의료 비용을 위해 돈을 저축함으로써 과세 신고 소득(비과세)을 줄이는 데 도움이 됩니다.

그러나 이 둘 사이에는 몇 가지 주요한 차이점이 있습니다.

일반적으로 FSA를 사용하면 전체 계획 연도에 대한 급여에서, IRS 요구 조건을 갖춘 의료비에 지출할 총 금액을 계획 연도 초에 결정할 수 있습니다. 결정된 비과세 자금은 연도별로 저축하고 지출해야 합니다.

주의해야 할 점은 본인이 예상하여 설정한 금액 중 사용하지 못한 금액은 환불받지 못합니다.

이것이 "쓰거나 또는 잃거나" 계정이라고 불리는 이유입니다. 그럼에도 불구하고 FSA는 계획 연도가 끝날 때까지 사용할 의료비 관련 비용을 절약하는 데 매우 유용합니다.

HSA는 FSA와 같이 IRS 요구 조건을 충족하는 의료비에 사용되어야 하지만, 이것이 FSA 보다 더 장기적인 계좌입니다. HSA는 IRS 자격을 갖춘 고공제 건강플랜(HDHP)의 적용을 받는 모든 사람이 이용할 수 있다. HDHP의 적용을 받는 한, 당신은 연간 최대 한도까지 당신이 선택한 증가분에 따라 당신의 HSA에 일년 내내 기여할 수 있다.

HSA 자금은 HDHP 플랜을 탈퇴하더라도 은퇴를 포함하여 사용할 때까지 사용할 수 있습니다. 그리고 65세 이후에는 그 자금을 무엇이든 사용할 수 있습니다. 국세청 자격을 갖춘 의료비에 대해서는 세금을 내지 않지만, 기타 모든 비용은 소득으로 과세됩니다.

몇 가지 차이점이 더 많은 차이점:

FSA는 고용주가 후원하는 계획이고, HSA는 개인이 보유합니다. 따라서 고용주를 바꿀 때 HSA를 가져갈 수 있지만, 일반적으로 FSA에 기여한 모든 자금은 사용되어야 하며, 사용하고 남은 금액은 고용주에게 반환됩니다.

HSA는 고용주와 상관 없이 개설할 수 있습니다.

만약 HSA 자격을 갖춘 건강 보험이 있다면 HSA에 돈을 축적할 수 있습니다.

HSA는 사용하지 않으면 없어지는 돈이 아닙니다. 사용하지 않은 자금은 은퇴할 때까지 매년 HSA에 남아 있습니다.

반대로 FSA의 경우 연말(또는 고용주가 제안한 이월 유예 기간)까지 돈을 지출해야 합니다.

만약 비축할 비용을 증가시키거나 더 적은 금액으로 변경할 필요가 있다고 결정한다면, HSA는 일년 내내 언제든지 변경할 수 있습니다. 반면 FSA는 계획 연도의 시작 시점에 설정되어 특이한 경우를 제외하고는 변경할 수 없습니다.

HSA는 최소한의 금액을 현금 계좌에 보관하고 나머지는 뮤추얼 펀드 등에 투자할 수 있습니다.

HSA를 사용하면 사용한 비용을 처리할 수 있는 기한이 무제한입니다. 언제든지 적절하게 사용한 비용에 대해 그 비용을 인출할 수 있습니다.

FSA의 경우 IRS 요구사항에 따라 적격한 비용을 입증하기 위해 마감일까지 영수증을 제출해야 합니다.

개인 각각의 건강 관리를 위해 필요한 사항들과 보험 계획을 정확히 이해해야, HSA와 FSA 중 어느 것이 나에게 적합한지 결정할 수 있습니다.

두 가지 모두 적합할 수도 있습니다. 이 경우 일반적으로 FSA는 치과, 시력 또는 부양가족 관리와 같은 특정 한 필요에 대한 "제한된 목적"의 FSA가 될 수 있습니다.

[추가: 20230119]

만약 직장을 퇴사하거나 은퇴한다면 고용주들은 당신이 FSA에서 쓴 돈을 돌려달라고 요구할 수 없습니다.

이는 계획 연도가 시작되는 즉시 계정 자금을 모두 사용할 수 있도록 보장하는 균일 보장 규칙(Uniform Coverage rule) 때문입니다.

단, 퇴사하는 순간 사용하지 않는 모든 FSA 금액은 고용주에게 반환됩니다.

What’s the Difference between an HSA and an FSA?

Ferne Emery, Account Manager, Pinnacle Health & Benefits

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) both help you reduce your taxable income by putting money away for healthcare expenses. However, there are some major differences between the two.

Generally speaking, an FSA allows you to elect at the beginning of a plan year the total that you want to set aside from your pay for the whole plan year to spend on IRS-qualified healthcare expenses. The tax-exempt funds are saved and spent on a year-by-year basis. This is why they are referred to as “use-it-or-lose-it” accounts. FSAs are great for saving funds you know you’ll use by the end of the plan year.

An HSA is also to be used for IRS-qualified healthcare expenses, but it is a longer-term account. HSAs are available to anyone covered by an IRS-qualified high deductible health plan (HDHP). As long as you are covered by an HDHP, you can contribute to your HSA throughout the year in whatever increments you choose, up to an annual maximum.

The HSA funds stay with you, even if you leave the HDHP plan, until you spend them – including through retirement. And after age 65, you can use the funds for anything at all. You won’t pay tax on IRS-eligible healthcare expenses, but any other expenses will be taxed as income.

A few more differences:

FSAs are employer-sponsored plans, and HSAs are owned by you. Therefore, when you change employers, you can take the HSA with you, but any funds contributed to your FSA generally must be spent.

You can open an HSA even if it isn’t offered by your employer. You’re allowed to contribute to an HSA as long as you have an HSA-eligible health insurance policy.

HSAs are not “use it or lose it.” Unspent funds remain in an HSA, year after year through retirement.

With FSAs, you must spend the money by the end of the year (or carryover period, if offered by your employer).

You can change your regular contribution amounts to your HSA at any time throughout the year if you decide you need to put away more or less. FSA contributions are set at the beginning of the plan year and cannot be altered except in cases of a qualifying event.

You can invest HSA funds. You can keep a minimum amount in the cash account and then invest the rest in mutual funds to grow over the long term.

With HSAs, you have an unlimited amount of time to reimburse yourself. You can withdraw the money for eligible expenses at any time.

With FSAs, you must submit receipts by a deadline in order to substantiate the expenses as eligible per IRS requirements.

Your healthcare needs and insurance plan will help determine whether an HSA or FSA is the best fit for you.

You may even be suited for both, in which case the FSA would be a “limited purpose” FSA for specific needs like dental, vision or dependent care.

Ferne Emery is an account manager with Pinnacle's Health & Benefits team. She is located at Pinnacle's Premier office in High Point, NC, and can be reached by phone at (336) 881-3209 or by email at Ferne.Emery@pnfp.com.

'미국 생활' 카테고리의 다른 글

| [미국 생활] Lifetime Income (Annuity) (0) | 2023.02.14 |

|---|---|

| [미국 생활] 은퇴 자금 저축 우선 순위 (0) | 2023.02.13 |

| [미국 생활] Small Business 세금 신고를 위한 영수증 종류 (0) | 2023.01.17 |

| [미국 생활] MUD Tax? 진흙 세금? 아닙니다 (0) | 2023.01.16 |

| [미국 생활] 항공권 발권에 있어서 Ticketing Carrier와 Operating Carrier 구분이 중요한 이유 (0) | 2023.01.05 |

댓글